I. Introduction

Corporations and operating entities own real property assets in the United States valued at multi-trillions of dollars.[1] Real estate, including leaseholds, generally account from 20% to as much as 40% of the total assets of a company.[2] Corporate real estate assets are often underutilized and overlooked as sources of funds in budgeting and planning.

This presentation examines the merits and cautions of sale-leaseback transactions, which allow businesses and users to enjoy the use of real property without the burdens and limitations of ownership.[3] In exchange, investors or purchasers of real property with the seller’s lease enjoy predictable returns with well-defined risks and low operational obligations.[4]

A “sale-leaseback” is defined as the sale of a real property asset and concurrent leasing back of the real property to the selling corporation or entity for the defined term of use.[5] Sale-leaseback transactions benefit long-term business financing and enables sellers to: (1) reduce occupancy costs; (2) improve their balance sheet; (3) maintain long-term control of property; (4) reduce risk; (5) diversify their portfolio; (6) avoid owning “bad dirt”; and, (7) improve returns by liquifying capital tied up in real estate ownership.[6] Sale-leasebacks also free up capital to earn increased margins obtained from inventory sales with multiple turns.[7]

At least three parties are generally present in a sale-leaseback transaction: the seller-lessee, usually a holding or subsidiary entity, chain or retail store, or national or international company; the purchaser-lessor, usually a real estate entity formed specifically to own the real estate; and the lender, typically an institution, such as a bank, insurance company, pension fund, real estate investment trust, or private investor, who supplies financing of the transaction. A purchaser may also use all equity or like-kind exchange funds to acquire the property. Seller-lessees may be enterprises, which are experiencing rapid growth or those with real estate assets needed to increase cash flows or liquidity.

The security of a sale-leaseback is the ownership of the real property, the improvements thereon, and the leased fee interest. Likely candidates for this transaction and financing include office buildings, free standing buildings, retail centers, operations and manufacturing facilities, existing properties, and properties with improvements, including those under construction.

Sale-leaseback transactions provide tax advantages to sellers, including the annual expensing of rental payments and occupancy expenses, which reduces income at a greater rate when compared to deducting interest on debt service and longer-term depreciation and amortization from owning the real estate asset.[8] These transactions also provide greater losses and benefits to the parties, with generally less equity encumbered and required from the buyer than traditional debt financing.

A successful sale-leaseback transaction uses lease financing as another source of private placement funds. The seller realizes 100% of sale-leaseback proceeds as compared to proceeds from a traditional financing debt-equity ratio of 80%/20%. This transaction is an attractive alternative to mortgage financing, especially when real estate values appreciate, and capitalization rates and market returns to investors are low.[9]

A sale-leaseback maintains flexibility by ensuring the seller/lessee the contractual right to use the property for its projected useful life as expressed in the lease term and options to extend or renew. Converting seller’s fixed assets into cash for working capital: (1) improves liquidity; (2) reduces debt; (3) allows investments to diversify assets; (4) provides greater margins from inventory or other more liquid assets; and (5) allows more favorable tax treatment. A knowledgeable buyer will ensure the lease provides the seller-lessee with pay for the day-to-day expenses of managing and operating the property during the lease term. Allocating utility payments, insurance, maintenance, and property taxes to the seller-lessee while occupying the building under a triple net or absolute net lease protects returns to the buyer. Benefits to the purchaser-lessor include income streams from the lease, depreciation, potential tax credit and deferral incentives, and appreciation accruals to the residual value of the real estate. The equity investor/buyer’s ownership role is passive on absolute net leased properties.

After the owner’s mortgage is satisfied, cash flow from the lease payments is unencumbered and becomes the lessor’s residual income on his purchase and investment, together with appreciation in value through market forces and inflation. Depending upon the tenant’s creditworthiness, remaining lease terms, and market conditions, the owner may re-finance the property to withdraw the debt’s tax-free, lump-sum cash proceeds.

II. The Typical Transaction

A sales-leaseback may be assembled by a team of in-house professionals, including attorneys, CPAs, financial advisors, and other tax or real property specialists.[10] If a firm does not have ready access to these specialists, they may turn to outside brokers, advisors, or consultants to assist in structuring the transaction.[11] The underlying lease in a sale-leaseback may be negotiated between the parties, but often proposed lease terms may be packaged in advance to determine the price-ask process part of the sale.

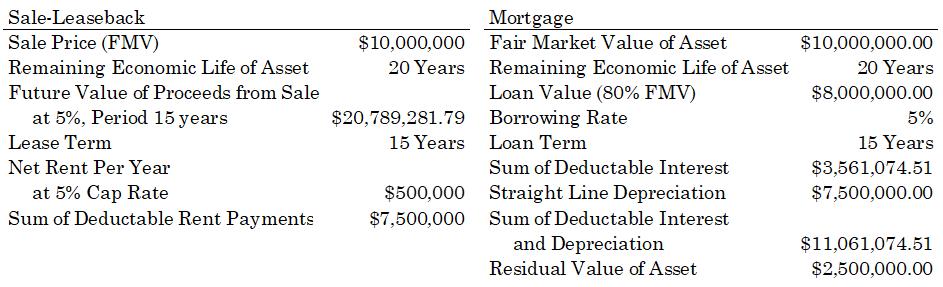

Below is a simple illustration of a sale-leaseback transaction as compared to a traditional mortgage on the same property. Some of the terms introduced above are not illustrated in this example. Utility expenses, taxes, insurance, and property maintenance expenses are not subtracted from the proceeds of the sale, nor shown as a deduction. These costs may qualify as expenses if the seller is required to make those payments under the terms of the lease.[12] Unless these expenses are capped, or the lessor retains the obligation to pay these expenses under the terms of the lease, these expenses should be equal and wash out[13] regardless of whether the seller sought a sale-leaseback or mortgage.

.png)

Regardless of who structures the transaction, sale-leasebacks follow a general framework. The seller-lessee identifies the property best suited for a sale-leaseback transaction it owns and needs for continued use. A purchaser is located, and a special purpose entity is formed, usually a limited liability company, to hold title to the defined-term, net leased property. The purchaser finances the acquisition price through long-term debt and equity, proceeds of a like-kind exchange, or partial seller financing. Once the purchaser-entity suitably finances the transaction, the property is leased back to the seller-lessee for continued possession and use for the defined term. The creditworthiness of the seller-lessee will be critical to the lender in underwriting, pricing, terms, and funding the loan.

Generally, two types of sale-leaseback financing are prevalent. First, there are tax or corporate credit-based transactions, which depend on the borrower/tenant’s corporate credit rating. Long-term mortgage bond financing with limited equity is another form of taxation or corporate credit-based sale-leaseback transactions, which can be more favorable for corporations when compared to alternative sources of funding. The sale-leaseback allows the greatest realized value for an asset as determined by rentals the seller pays as the buyer’s expected rate of return.

Another form of sale-leaseback financing is more traditional and typically involves a smaller, privately-held company with access to equity and institutional funding. Borrowing proceeds of approximately 75% to 80% equity/debt ratio is normal, with 20% to 25% of owner/investor equity required. Rental costs are typically higher, and leases tend to carry 10 to 20 years terms. Unlike traditional debt financing, this transaction still allows the seller to realize 100% of an asset’s value. Additionally, the transaction costs of sale-leasebacks may be lower than with debt financing, particularly if multiple properties are bundled for sale with retained leases.

The net present value of rental streams for the early years of the lease term may be set at less than or equal to (≤) typical debt service costs for the same period. Doing so compels the buyer/lessor to consider and account for tax benefits and market appreciation as a portion of his initial return on the investment. By offsetting costs via the tax benefits of ownership, the initial subsidized or below market rents paid by the seller-lessee may be less than traditional debt service.

Rental increases after the first three to five years into the term will allow rents to exceed debt service costs gradually. The time value of money in a sale-leaseback can be equity contributed by the buyer, which may lower the effective rent to the seller lessee during the early years.

This is observable in the above example. The aggregate rental payments made by a seller under a sale-leaseback arrangement are several million dollars less than the aggregate debt service costs of a comparable mortgage. One key difference in the example is that a sale-leaseback transaction allows the realization of 100% of the fair market value of the real estate asset to the seller, while the mortgage only permits the realization of 80% of the fair market value to the debtor.

The seller-lessee must remain cognizant of the tax implications of a sale compared to traditional financing. Not only is rent deductible, but other expenses paid under a net lease may also be deductible.[14] Utility payments, taxes, or other maintenance expenses required under the lease may serve to minimize the seller-lessee’s tax burden, but also offset the proceeds recognized by the sale in a sale-leaseback. Sellers must consider whether to recognize a gain or loss on the property because of the sale, whereas traditional financing leaves the putative seller with a real estate asset with residual value.

III. Protecting the leasehold

The seller-lessee in a sale-leaseback transaction is subject to primary non-owner risks: (1) failure to record the memorandum of lease, which allows a bona fide purchaser without record notice to take property free and clear of the lease; (2) subordination of the lease to the buyer’s financing, even if the lease is prior in time, which could eliminate the seller-lessee’s interest in foreclosure; and, (3) failure to actively protect the leasehold in the event of the lessor/buyer’s bankruptcy.

Prior to memorializing and recording a lease, bilateral risks arise in contract drafting and interpretation. Leases, similar to other contracts, are to be interpreted based on the plain language and meanings of words used in the lease.[15] Disputed or ambiguous terms of a lease may be construed against the party who drafted the document.[16] In Columbia East Associates v. Bi-Lo, Inc., the court stated, “[w]here the contract is susceptible of more than one interpretation the ambiguity will be resolved against the party who prepared the contract.”[17] The terms of the lease must be stated in clear and unambiguous terms before the sale of the property.

A threshold concern for a seller-lessee is whether the lease was lawfully memorialized and recorded, protecting the seller-lessee from successors-in-interest claiming superior rights. North Carolina’s Statute of Frauds and the recordation statute, the Conner Act, states that all leases of three (3) or more years must be in writing and no lease or other conveyance of land for more than three (3) years shall be valid to pass any property interest as against lien creditors or purchasers for a valuable consideration from the donor, bargainer, or lessor but from the time of registration thereof in the county where the land lies.[18]

This statute has been interpreted to require the party asserting a superior right over the lease to be a bona fide purchaser for value.[19] Once the property is purchased for value,[20] leased back to the seller for use, and the transfer of said property is properly memorialized and recorded,[21] the seller-lessee has sufficiently placed would-be buyers on notice of their leasehold interest. Additionally, courts have preserved the seller’s leasehold interest when: (1) a successor to the buyer has actual prior notice of the seller’s leasehold interest and acted with fraudulent intent, or (2) where disclosure of the seller’s interest was mistakenly omitted from the recorded instrument.[22]

Another issue posed to sellers in a sale-leaseback transaction is the possibility of subordination of the lease to any of the buyer’s prior or subsequent financing. Subordination clauses within the sale-leaseback agreement can stipulate whether the lease is subordinate to other financing, such as mortgages, made prior to the leaseback.

In T.D. Bickham Corp. v. Hebert,[23] the Supreme Court of Louisiana determined the plain language within the lease agreement, stating “[t]his lease shall at all times be subject and subordinate to the lien of any mortgage or mortgages now or hereafter placed upon [the property]” was sufficient to subordinate the lease by Hebert.[24] Courts typically preserve and enforce the parties’ rights to contract as the parties therein agreed. However, in the event a lease includes the subordination of a prior and properly recorded interest, a foreclosure sale may eliminate the lease interest.

Another issue and risk for potential sellers/lessees occurs if a buyer/lessor files for bankruptcy, which may sever the seller’s lease on the property. Once an owner/buyer’s bankruptcy is instituted, the U.S. Code allows for the appointed bankruptcy trustee to reject unexpired leases of real property under which the debtor is the lessor.[25] This Bankruptcy Code provision may result in a scenario in which the seller’s interest could be wiped out, if classified as a lesser interest.

Sellers with an unexpired lease are moderately protected through two options: (1) treat the rejection as a termination of the lease and assert damages, or (2) continue occupancy of the premises, continuing to pay rent, and offsetting the value of any damages caused by the buyer’s nonperformance. When the seller treats the rejection as a termination, the seller is permitted to depart the premises and to file claim for damages against the bankruptcy estate as is customary in contractual breach.[26] The seller/lessee must then ensure sales by the trustee are in compliance with 11 U.S.C. § 363(f) and objected to by the seller/lessee after being placed on notice of such sale.[27]

In the latter scenario, the Code permits the lessee to remain on the premises and offset their rent by damages, not beyond total rent, through the lessor’s nonperformance occurring after said rejection of the lease.[28] The Code also protects the lessee’s rights to any renewal or extension of interest.[29]

IV. Distinguishing Sale Leaseback Transactions & Secured Financing

Sale-leaseback transactions may also incur negative tax consequences if the Internal Revenue Service (“IRS”) of the United States Treasury categorizes the transaction as a financing or sham transaction, rather than a true arms-length, sale-leaseback transaction.[30] This re-characterization deems the seller as the owner of the property for income tax purposes, and requires sellers to depreciate the improvements on the property.[31] The seller cannot expense the full amount of rental payments paid to the buyer and other expenses. Losing these tax benefits reduces the appeal and returns of a sale-leaseback.[32]

A. Frank Lyon Co. v. United States

An illustrative attempt by the IRS to adversely re-characterize a sale-leaseback transaction is found in Frank Lyon Co. v. United States.[33] In Frank Lyon, a bank entered into an agreement with a director/investor, in which the investor would take title to a new bank building, while it was under construction. The investor/buyer simultaneously leased the building back to the bank. The investor/buyer obtained a construction loan and mortgage for the building. The bank retained repurchase options throughout the term of the lease; the options were equal to the sum of any unpaid balance on the mortgage and the investor’s original investment in the property plus interest.

When the investor/buyer claimed deductions for the depreciation of the building and interest paid on the mortgage loan on his federal income tax return, the IRS denied the deductions. The IRS claimed the investor/buyer was not the owner of the building for tax purposes, and asserted the sale-leaseback was, in fact and substance, a financing transaction.

The Supreme Court ruled upon the distinction between the two, stating where:

There is a genuine multiple-party transaction with an economic substance which is compelled or encouraged by a business or regulatory realities, is imbued with tax-independent considerations, and is not shaped solely by tax-avoidance features that have meaningless labels attached, the [g]overnment should honor the allocation of rights and duties effectuated by the parties. Expressed another way, so long as the lessor retains significant and genuine attributes of the traditional lessor status, the form of the transaction adopted by the parties governs for tax purposes. What those attributes are in any particular case will necessarily depend upon its facts.[34]

The Court identified key factors, which tended to categorize this transaction as a true sale-leaseback, including an arms-length transaction; the investor was liable for the mortgage loan; the investor alone accounted for the mortgage on its balance sheet; and the repurchase options were not guaranteed. The investor bore the risks of this transaction and reduced his borrowing capacity by disclosing the debt liability on his financial statements.

The Court assessed the economic realities and substance of the transaction, rather than the form the parties used. While the accounting and tax treatment of sale-leasebacks has changed in the years since the Court’s holding, Frank Lyon remains the seminal case concerning sale-leaseback transactions and interpretation.[35]

B. Sacks v. Comm’r

A second example of a proper sale-leaseback is Sacks v. Comm’r, in which the United States Court of Appeals for the Ninth Circuit applied the rule from Frank Lyon.[36] Mr. Sacks invested in solar water heaters purchased by BFS Solar Incorporated. BFS sold each heater to investors for $4,800. Each heater was then leased to homeowners for installation. The investors were given a base rent and would receive a percentage of what homeowners paid for installation. The investors paid $2,400 cash and $2,400 pursuant to a ten-year, 9% note on which they would be personally liable on each note. Homeowners leased the units for 24 months, paid no rent for this period, and then would decide whether to continue leasing the unit. BFS estimated that the leases would cost less than a conventional electric water heater.

After Mr. Sacks claimed depreciation and investment tax credits, the IRS disallowed the credits on the grounds that the sale-leaseback was a sham. The IRS determined the transaction was a financing device dressed up as ownership. The Tax Court agreed, but the Court of Appeals reversed. The transaction was not a sham because Mr. Sacks retained a personal obligation to pay for the heaters, Mr. Sacks had paid fair market value, the tax benefits would have existed for either BFS or Sacks, and the business was genuine.

The sale-leaseback transaction carried practical economic effects: Mr. Sacks had a business purpose outside of simply accruing tax benefits, and the transaction shifted the speculative risk from BFS to Sacks. Although Mr. Sacks was unlikely to make a profit but for the tax benefits, favorable tax consequences are not a reason for disallowing transactions in which tax benefits are an investment consideration.[37] Mr. Sacks retained significant risks and the benefits of ownership. His capital was committed and remained at risk.

C. Golden State Lanes v. Fox

An illustrative example of a transaction held not to be a legitimate sale-leaseback and held instead to be a financing transaction is found in Golden State Lanes v. Fox.[38] Golden State had agreed to a 20-year lease at a rent of $1,050 per month. As a condition of the lease, Golden State was required to remodel the property. After spending $100,000, an additional $150,000 was required to complete the work.

The Fox Group provided funding via a $1,000 payment to Golden State and a $149,000 payment to a Beverly Hills bank for Golden State’s pre-existing obligations. Golden State in turn assigned their lease to Fox, who subleased the property back at the previous rent plus an additional $2,500 per month for an 8-year term, an effective interest rate and return of 20% to Fox with no prepayments allowed.

Golden State was provided repurchase options requiring additional premiums of 100% over the principal at two years, and 50% over at four years. Chattel mortgages or UCC financing statements over all fixtures were filed in favor of the Fox Group. The individual stockholders of Golden State unconditionally guaranteed performance and to indemnify Fox. Upon default, Fox retained the right to enter the premises and take possession of all fixtures and equipment, and to terminate all rights under the contract.

Golden State attacked the transaction as usurious under California law, which at that time limited lawful interest rates to a maximum of ten percent (10%). Golden State was bound to repay the identical sum advanced by Fox, with 20% non-prepayable interest, and Fox was bound to reconvey the property to Golden State at the end of the lease term. Fox would not retain any residual value in the property. The underlying lease payment/interest rate was twice the legal maximum. The court looked past the form of the transaction and reviewed its substance. The court found this transaction was in fact a loan of money, even though it was structured as a sale-leaseback of real property. “A contract in the form of a sale with an option to repurchase is treated as a loan where the contract is simply a cloak to cover up a scheme to collect usurious interest.”[39] The court held the “heart and purpose” of the transaction was to transfer money with a non-cancellable obligation to repay a debt with a usurious interest rate.[40]

V. Financial Accounting Standards Board

The Financial Accounting Standards Board (FASB) establishes standards of generally accepted accounting principles (“GAAP”) for the purposes of federal securities laws.[41] These standards are applicable to public companies and any to other entities, which file financial statements with the United States Securities and Exchange Commission (SEC).[42]

The 2016 accounting standards issued by FASB provide additional guidance on structuring a legally valid sale-leaseback.[43] These revised standards may have a significant impact on the tax treatment of sale-leaseback transactions.[44] A sale-leaseback may fail if either the sale or the leaseback portion of the transaction is not compliant with FASB ASC 842.

For a transfer of assets to be considered a sale in a sale-leaseback transaction, compliance with ASC 606 is required.[45] Seller-lessees can treat a transfer of assets as a sale if a contract exists[46] and the seller satisfies their performance obligation by transferring ownership and control of the asset.[47] If a leaseback is classified as a finance lease or a sales-type lease by the buyer-lessor, the leaseback portion of the transaction fails and control of the asset is not deemed to have transferred.[48] Without a sale-transferring ownership of the asset, neither the seller or buyer can account for the purchase as a sale-leaseback transaction. Consideration paid for the asset is accounted for as a financing transaction.[49]

ASC 842 also specifies that repurchase options preclude sale-leaseback accounting, unless the asset is nonspecialized, and the price of the option is the fair value of the asset on the date the re-purchase is exercised.[50] This standard prohibits a “bargain basement” or a pre-determined nominal or below market re-purchase price at the end of the lease.

Under the new standards, certain real estate transactions not previously considered a sale-leaseback may now qualify for sale-leaseback accounting, while transactions involving assets other than real property that was previously qualified may no longer qualify for sale-leaseback accounting.[51]

When determining whether to structure a transaction as a sale-leaseback, please note that the old standards applied only to lessees and included a detailed and specialized guidance for accounting and reporting real estate sale-leaseback transaction. The new standards apply sale-leaseback accounting to both lessees and lessors and do not provide such prior guidance.[52]

VI. Operating v. Financing Leases

The distinction between operating and financing leases was retained under the FASB 2016 amended standards.[53] Seller/lessees will now need to recognize virtually all leases on their balance sheets.[54] Unlike the previous standard, ASC 842 requires lessees to recognize lease assets and lease liabilities for leases classified as operating leases.[55] FASB however retains the practice of classifying leases for income statement purposes.[56] Lessees classify leases as finance or operating leases, but the classification criteria are substantially similar to the old standards for classifying leases as operating or capital leases.[57]

A lessee must classify a lease as a finance lease if: (1) the lessor is bound to reconvey the property to the lessee by the end of the term; (2) the lease grants a repurchase option the lessee is reasonably certain to exercise; (3) the lease term is for the major part of the remaining economic life of the property; (4) the present value sum of the lease payments and any residual value guaranteed by the lessee not reflected in the lease payments equals or exceeds the fair value of the underlying asset; or, (5) the asset is specialized and there is no expected alternative use for the lessor at the end of the term.[58] If none of these criteria are met, the lessee must classify the lease as an operating lease.[59]

ASC 842 provides guidance on classifying leases.[60] Seventy-five percent or more of the remaining economic life of an asset may be considered a major part of the asset’s remaining life. Lease commencement dates within the last 25% of the total economic life of the asset are at or near the end of the asset’s economic life.

Ninety percent (90%) or more of the fair value of the underlying asset is considered to equal substantially all of the asset’s fair value. In effect, aggregate rent payments amounting to 90% of the fair value of the asset, made over three-quarters of the remaining life of the asset, would constitute a lease term for most of the remaining economic life of the property. Under FASB standards, this regime would be categorized as a financing lease, not an operating lease.[61]

ASC 842 requires lessees to recognize virtually all leases on their balance sheets and removes one of the prior advantages of sale-leaseback transactions. Sale-leaseback transactions no longer provide seller-lessees off-balance sheet financing. Many other advantages of a sale-leaseback transaction nevertheless remain applicable. These transactions free up cash values otherwise invested in illiquid real estate assets, are an alternative and effective financing vehicle for seller-lessees, the tax benefits remain largely unchanged, and balance sheets are still strengthened by reflecting lower debt.

VI. How Mortgage Debt Benefits and Burdens

There are cautions and drawbacks to sale-leaseback transactions, which should be considered and cannot be ignored when determining whether to structure a transaction as a sale-leaseback or a traditional mortgage. The new buyer/lessor/landlord and seller/lessee/tenant relationship gives rise to many of these issues. The seller may lose flexibility in the long-term control to modify or expand the property, is locked into a long-term lease, relies upon the buyer/lessor for some upkeep of the property, retains no residual interest in the property at the expiration of the lease, bears the risk of landlord bankruptcy, and may pay more in rent than the amount of the carrying costs of debt on the property would have been.

Lessees generally lose the right to make structural modifications and expansions without owner/lessor consent.[62] Financing for these modifications and expansions may not be externally available and must be internally generated from lessee’s reserves or cash flows, unless lessor is willing to finance modifications and improvements through a lease amendment.

Buyers/lessors also face risks in every transaction. Despite the valuable tax benefits of a sale-leaseback, the buyer-lessor still faces: (1) deterioration of the lessee’s credit; (2) delay or disallowance of tax benefits; (3) unexpected or early lease termination; (4) investor’s need for greater liquidity; (5) change in investor’s tax bracket; (6) mergers and closures of the property; and, (7) rejection of the lease in bankruptcy.

If the property is a single tenant, net leased property, all the buyer’s equity value, above the residual value of the unoccupied improvements and land, is at-risk. Suppose the capitalized rate of return rental is higher than the market lease rates, and a breach of lease occurs. In that case, a significant write-down in expected returns must occur to get the property re-occupied with a performing tenant. When determining whether traditional debt servicing or a sale-leaseback is appropriate, reviewing courts may turn to who bears the burden of risks when determining whether a transaction is a true sale-leaseback or disguised financing.[63]

Mortgage debt gives the owner control and asset appreciation, but at a higher cost than a sale-leaseback, allowing only 75-80% of the property’s value to be realized. Also, the value of the dirt below the improvements cannot be depreciated by the owner. With the new ASC standards, both sale-leasebacks and mortgage debts are reported as a balance sheet liability, but are not necessarily treated the same.[64]

A sale-leaseback transaction may offer a more effective cost of financing, possibly at 200 to 300 basis points below the company’s cost of the mortgage debt and avoided fees and costs. The seller must determine the internal rate of return of rentals to be paid under the lease. The rate of the rental capitalized and the comparable market will necessarily be a dominant factor to arrive at the value of the asset, and consequently its selling price.

Financing and equity remain important factors in sale-leaseback agreements. Sale-leaseback lenders usually finance up to 90-100% of the purchase price versus a more traditional figure of 75-80% real estate value for debt/equity financing. Additionally, 75-80% debt/equity is more typical of ten-to-twenty-year lease terms. The key to the best financing is to have debt additionally secured by the seller/lessee’s corporate credit through a separate unconditional guaranty agreement of the lease by the seller or its parent company.

Required equity for fees and a rate buy-down in traditional financing range from 1 to 10% with good corporate credit. An additional 20-40% of the purchase price is spread between rent and debt costs during the early years of the lease term vis-a-vis rent subsidies. In a sale-leaseback, the buyer’s return may include tax benefits in early years with lease payments subsidized at less than or equal to the mortgage payments. Cash flows during later years, and sale/refinancing proceeds of the asset may occur at an appreciated value when the occupancy/use by the seller/lessee is completed, or the lease term is renewed at a higher rate.[65]

Financing with a loan has a direct impact on lease terms. Debt service cost is a major component of rent-minimized debt service yielding lower rent costs. Conventional debt held over 20-to-25-year lease terms with interest-only payments during the early years will lower debt service costs and increase cash flows. Lower interest on debt payments balances lower corporate rentals in early years. Greater principal payments in early years result in fewer tax benefits, more equity invested, and higher rental costs that might be used more profitably in other assets.

Financing by segmenting or stripping the debt can also lower borrowing costs and rentals. A combination of varying term debt instruments of ten, fifteen, twenty, and twenty-five years result in lower rates for short maturities as compared to conventional 25-year debt. A larger market of potential lenders helps produce a more competitive market. Consequentially, lower-available interest rates on comparable loans may also lower the capitalization rates offered by the seller and be used to set the rentals in the lease.

The cost of sale-leaseback valuation is determined by the internal rate of return or implied interest costs of the rental stream during the lease term. Another difference between traditional financing and sale-leaseback transactions is the contrast between the internal rate of return on lease payments and the debt rate due to the sale or retention of tax credits, depreciation, and interest deductions.[66]

VII. SILO Transactions

A related transactional structure to a sale-leaseback is a sale-in, lease-out (SILO). SILO transactions also seek to shift and transfer tax benefits associated with property ownership from one party to another, typically from a tax-exempt entity to a taxpayer. In reality, these transactions fail to transfer the benefits and burdens of ownership in the underlying property. The IRS has characterized, and courts have held via application of the substance-over-form doctrine developed in Frank Lyon, purported sale-leaseback transactions are nothing more than variants of a SILO transaction.[67]

Most SILO transactions are similarly structured.[68] A tax-exempt entity first leases an asset to the taxpayer under a headlease for a term that exceeds the useful life of the asset, which qualifies as a sale for federal tax purposes. The taxpayer concurrently subleases the property back to the tax-exempt entity for a term less than the useful life of the asset. This is typically an absolute net lease. Each sublease contains a repurchase option, fully funded by the taxpayer’s original “purchase” price under the headlease.

The taxpayer prepays its entire rent under the headlease in a lump sum at closing. This payment may be funded entirely by taxpayer equity or in part by taxpayer equity and in part by a non-recourse loan. The prepaid “rent” is deposited into restricted accounts, nominally held by the tax-exempt entity, but are pledged to pay the entity’s rental obligations and to fund the repurchase option. A four to eight percent portion of the payment is paid to the tax-exempt entity as an accommodation fee for participating in the transaction.

The equity portion of the headlease payment is invested in high-grade debt, typically government bonds. The investment is managed to ensure the tax-exempt entity maintains funds to repurchase the asset. The exercise/option price is set at the beginning of the transaction.

SILO transactions typically maintain alternatives in the unlikely event that the tax-exempt entity chooses not to exercise the repurchase option.[69] The taxpayer may take control of the asset, seek a third party to continue using the asset, and may have predetermined and stipulated damages. The burdens on the tax-exempt entity of not exercising the option are typically structured such that there is a high likelihood of the option being exercised.[70] The options generally ensure a fixed return on the investment, and the taxpayer retains no risk.

SILO transactions offer tax benefits to the taxpayer. The taxpayer may take depreciation on the asset, deductions for interest payments made on loans to finance the headlease prepayment, and write-off transaction costs.[71] The tax-exempt entity retains the accommodation fee. The tax-exempt entity retains all the burdens and benefits of ownership. The taxpayer seeks a fixed, predictable return on investment with no risk.

No money except for the initial accommodation fee actually changes hands. The debt portion of the sublease payments is fully funded, and the taxpayer’s debt is effectively defeased. The taxpayer typically ignores the non-recourse loan debt on its balance sheets.

These transactions are, in essence, a taxpayer pre-purchasing tax benefits for a fee from a tax-exempt entity that cannot use those deductions, dressed up like a real property transaction. SILO transactions are often viewed as violative of the substance-over-form doctrine and have largely been held by courts to be abusive tax shelters.[72] SILO transactions in substance are a circular exchange of money.

The United States Court of Appeals for the Seventh Circuit reviewed and addressed SILO transactions, which purchased tax deductions elevated in form and disguised as sale-leasebacks. In Exelon Corp. v. Comm’r,[73] Exelon sought to conduct like-kind exchanges on power plants via six sale-leaseback agreements. After selling real estate for $2 billion more than its estimated value, Exelon sought to minimize taxable gain from these transactions. In the “sale-leaseback” transactions, Exelon leased an out-of-state power plant from a tax-exempt entity for longer than the estimated life of the plant. Exelon concurrently leased the property back for less than the economic life of the plant. Each tax-exempt entity received a multi-million-dollar accommodation fee, and a fully funded purchase option to terminate Exelon’s interest at the end of the sublease. The U. S. Tax Court agreed with the Commissioner to deny the sale leaseback treatment of the transactions.

The Court of Appeals affirmed the tax court’s decision, holding the Exelon transactions in substance resembled loans from Exelon to the tax-exempt agency. Exelon never acquired ownership of the replacement plants. The tax-exempt entities retained the right to uninterrupted use, enjoyment, and possession of the properties. The subleases were absolute net leases, and the entities were responsible for the costs and expenses associated with ownership.

The repurchase options were structured so that exercise of the options was “reasonably likely”; the burden of not exercising the option was high; and the option was already fully funded. The tax-exempt entity would not change their ownership position before the “transaction” closed, ensuring they would be millions of dollars richer.

Exelon tried to claim the special tax deductions that were “at the heart of SILO cases,” but the transactions were held in substance to be SILO’s.[74] The Court also upheld penalties levied against Exelon for underpayment of taxes due to Exelon’s negligence and disregard of the relevant and controlling tax rules and regulations when structuring the transaction.[75]

Conclusion

Advantages to the seller-lessee and buyer-lessors in sale-leaseback agreements are numerous. Possible cost/benefit disadvantages and risks cannot be overlooked. Future increases in real estate value accrues to the buyer-lessor. Lessees often retain most of the burdens of ownership, but not the freedom of action associated with ownership, i.e., a less marketable leasehold and limitations on future financing and expansion, modifications, or demolition of the improvements. Lessees must be vigilant to protect the priority of the leasehold through recordation, scrutiny of subordination provisions, and be pro-active to preserve the leasehold in the event the buyer/lessor files a bankruptcy petition.

The future of sale-leaseback financing depends upon potential legislation which may decrease or eliminate the tax benefits associated with this transaction. Longer depreciation periods, changes in tax rates and reporting methods, and financial reporting changes all affect values and impact the market for this transaction. The consequences of the 2016 FASB amendments have yet to be fully and practically examined.[76] These amendments may impact the decision of whether and how to structure and report a transaction as a sale-leaseback.[77]

In conclusion, sales-leaseback financing offers the seller/lessee the opportunity to realize 100% or more of the real estate asset’s value. These transactions provide the seller/lessee a long-term fixed cost option and favorable tax and balance sheet treatment as an operating lease, while retaining operating control of the property during the term and renewals of the lease.

When properly structured, the sale-leaseback offers the seller/lessee immediate expensing of the lease payments, as compared with the longer depreciation/amortization and interest deductions from owning the improved property. The buyer/lessor receives a fixed return on a traditionally appreciating real property asset with tax advantages and minimal burdens of ownership.

See, e.g., U.S. Census Bureau, Quarterly Financial Report: U.S. Corporations: All Manufacturing: Total Assets, FRED Economic Data, St. Louis FED (last visited March 3, 2021), https://fred.stlouisfed.org/series/QFR223MFGUSNO. The total assets owned by corporations labeled “manufacturing” alone total in the trillions, without including corporations whose primary business is mining, retail sales, information, or professional and technical services.

Theron R. Nelson et al., Real Estate Assets on Corporate Balance Sheets, 2 J. Corp. Real Est. 29, 29 (1999).

Brian C. Crist, Sujata Yalamanchili, & Scott Kadish, Look Before You Lease: An Overview of Sale Leaseback Transactions 1 (Feb. 22, 2021), https://cdn.ymaws.com/acrel.site-ym.com/resource/collection/95D55D5F-5F29-4C41-B78C-F9C7A8C4D34F/Yalamanchili - Sale Leaseback Transactions - 0.pdf.

Id.

A. Brant Bryan, The State of Sale-Leasebacks: What Corporations and Should Expect Today, J. Corp. Real Estate 1, 15-23, 19 (2003).

Id.

Nelson et al., supra note 2, at 29.

26 U.S.C.A. § 162(a)(3) (2022).

Crist, Yalamanchili, & Kadish, supra note 3, at 7-8 (explaining low capitalization rates may indicate sellers are demanding, and securing, higher purchase prices for their real property).

See, e.g., Frank Lyon Co. v. United States, 435 U.S. 561 (1978) (discussing how a sale-leaseback involving a bank choosing a Board insider to enable the transaction).

See, e.g., Exelon Corp. v. Comm’r, 906 F.3d 513 (7th Cir. 2018) (discussing how a large corporation relied on an outside firm to structure the purported “sale-leaseback”).

26 U.S.C. § 162(a)(3) (2022).

James Chen, Wash, Investopedia (last updated April 10, 2022), https://www.investopedia.com/terms/w/wash.asp.

26 U.S.C. § 162(a)(3) (2022).

Lowe’s of Shelby, Inc. v. Hunt, 226 S.E.2d 232, 234 (1976) (citing Kohler v. J.A. Jones Construction Co., 201 S.E.2d 728, 731 (1974)).

Columbia East Assoc. v. Bi-Lo, Inc., 386 S.E.2d 259, 261-262 (S.C. Ct. App. 1989).

Id. at 262.

N.C. Gen. Stat. §§ 22-2, 47-18 (2021).

John M. Tyson, Drafting, Interpreting, and Enforcing Commercial and Shopping Center Leases, 14 Campbell L. Rev. 3, 275-322, 277 (1992).

See Bona fide purchaser, Black’s Law Dictionary (9th ed. 2009).

See N.C. Gen. Stat. §§ 47-117, 118, 120 (2022).

Tyson, supra note 19, at 277.

432 So. 2d 228 (La. 1983).

Id. at 229.

11 U.S.C. § 365(h)(1)(A) (2020).

Id. § 365(h)(1)(A). See also John M. Tyson, Automatic Stays and Administrative Expenses: Rights and Remedies Available to Landlords and Tenants in Bankruptcy Proceedings, 31 Campbell L. Rev. 3, 413-430, 427 (2009) citing 11 U.S.C. § 365(h)(1)(A)-(B); Milstead v. Tele Media Broad., Inc. (In re Milstead), 197 B.R. 33, 35- 36 (Bankr. E.D. Va. 1996) (“Under § 365(g)(1), rejection of an unexpired lease by a debtor constitutes a breach of that lease prepetition. Accordingly, the non-debtor party to the lease becomes the holder of an unsecured prepetition claim.”).

11 U.S.C. § 363(f); see also Precision Indus. Inc. v. Qualitech Steel SBQ, LLC (In re Qualitech Steel Corp.) 327 F.3d 537 (7th Cir. 2003) (discussing how the court of appeals held Qualitech’s selling of its assets under 11 U.S.C. §363(f) extinguished Precision’s interests after Precision failed to timely object upon being placed on notice of Qualitech’s intent to sell the leased property through bankruptcy).

11 U.S.C. § 365(h)(1)(A)-(B) (2020).

Id.

See Crist et al., supra note 3, at 2-4.

See 26 U.S.C. § 168 (2022).

Crist et al., supra note 3, at 2.

See Frank Lyon Co. v. United States, 435 U.S. 561 (1978).

Id. at 583.

Id.

Sacks v. Comm’r, 69 F.3d 982 (9th Cir. 1995).

Id. at 987.

Golden State Lanes v. Fox, 232 Cal. App. 2d 135 (1965).

Id. at 139.

Id. at 141.

See Commission Statement of Policy Reaffirming the Status of the FASB as a Designated Private-Sector Standard Setter, 68 Fed. Reg. 23333 (May 1, 2003).

Id.

See generally Fin. Acct. Standards Bd., Accounting Standards Codification, No. 2016-02, Leases (Topic 842) (2016) [hereinafter “Leases (Topic 842)”].

Crist et al., supra note 3, at 4.

Fin. Acct. Standards Bd., Accounting Standards Codification, § 842-40-25-1 (2016) [hereinafter “FASB ASC”].

Id., §§ 606-10-25-1 through 606-10-25-8 (2016).

Id., § 606-10-25-30 (2016).

Id., § 842-40-25-2; See Section V infra.

Leases (Topic 842), supra note 43, at 6.

FASB ASC, supra note 45, § 842-10-25-2(d)(e).

Leases (Topic 842), supra note 43, at 6.

Id.

See Crist et al., supra note 3, at 4; FASB ASC, supra note 45, § 842-10-25-1 et seq. (2016).

Crist et al., supra note 3, at 4; Leases (Topic 842), supra note 43, at 1; FASB ASC, supra note 45, 842-30-45-1 et seq. (2016).

Leases (Topic 842), supra note 43, at 2.

Crist et al., supra note 3 at 4.

Id.

FASB ASC, supra note 45, § 842-10-25-2.

Id., § 842-10-25-3.

Id., § 842-10-55-2 (2016).

See id.

Crist et al., supra note 3, at 4-6.

See, e.g., Frank Lyon Co., v. United States, 435 U.S. 561 (1978). One of the determinative factors in the court’s analysis was that Lyon alone bore the risk on the notes to his lenders, which reduced his capacity to borrow by disclosing the liability on his financial statements.

FASB ASC, supra note 45, § 842-10-25-1 et seq. (2016).

See generally Stuart Saft, Com. Real Estate Forms 3d § 10:5 (Nov. 2020 update).

See, e.g., 35 Jean Taranto, Mortgage Liens in New York § 6:11 (2d ed. 2020).

See, e.g., Exelon Corp. v. Comm’r, 906 F.3d 513, 517-18 (7th Cir. 2018).

Id.; Wells Fargo & Co. v. U.S, 641 F.3d 1319 (Fed. Cir. 2011).

Exelon, 906 F.3d at 517-18.

See Wells Fargo, 641 F.3d. at 1328. In the SILO transactions at issue, the sublessees were “virtually certain” to exercise their options, and in several transactions this was expressly stated at the onset of the transaction.

Exelon, 906 F.3d at 517.

Wells Fargo, 641 F.3d at 1324.

Exelon, 906 F.3d at 517-18.

Id. at 524.

Id.

FASB ASC, supra note 45, § 842-10-25-1 through 25-7 (2016).

Id.